Apartment supply falls a further 12% - JLL

Contact

Jul 31, 2019

Apartment supply falls a further 12% - JLL

JLL data showed the number of apartments under construction in the inner-city regions of Australia’s six major capital cities fell a further 12% in 2Q19 to 39,660 apartments and was down 21% over the past year.

-

JLL AustraliaThe number of apartments under construction in Inner Sydney fell 17% to 10,230 in 2Q19 and is 40% lower than a year ago.

JLL AustraliaThe number of apartments under construction in Inner Sydney fell 17% to 10,230 in 2Q19 and is 40% lower than a year ago.

Apartment prices should stabilise in Q2 2019, but investor demand will remain muted as it will continue to be a tough environment for developers to commence new apartment projects, particularly large ones, according to JLL’s latest Q2 2019 Apartment Market Reports.

“It is fair to say that the recent recovery in housing market confidence has been quicker and stronger than expected," said JLL Head of Residential Research - Australia, Leigh Warner.

"A stabilisation of dwelling prices will also undoubtedly be good for consumption and the stabilisation of the broader economy. However, we shouldn’t get too carried away about any sudden rebound in the apartment market, construction in particular.

"Investors are still a large portion of apartment demand and neither offshore nor domestic investor demand are likely to rebound strongly any time soon. This will keep pre-sales rates relatively slow and mean it will stay tough for developers to reach pre-commitment hurdles required for finance and few projects will proceed to construction,” said Mr Warner.

At a glance:

- Apartment prices should stabilise in Q2 2019, but investor demand will remain muted as it will continue to be a tough environment for developers to commence new apartment projects, particularly large ones, according to JLL’s latest Q2 2019 Apartment Market Reports.

- The total number of apartments in the supply pipeline at all stages of development that JLL track is 21% lower over the past year and a massive 46% below its late-2016 peak.

- JLL Head of Residential Research - Australia, Leigh Warner said the bottom line is that the number of apartments being built will continue to fall for some time yet and will fall below the level of underlying demand from population growth. This will allow the market to catch up and fully absorb recent strong construction levels.

JLL data showed the number of apartments under construction in the inner-city regions of Australia’s six major capital cities fell a further 12% in 2Q19 to 39,660 apartments and was down 21% over the past year.

Perhaps showing a little optimism on the part of developers, the number of apartments being marketed across the monitored markets rose 7% in the quarter but is still 34% lower over the past year.

Additionally, the total number of apartments in the supply pipeline at all stages of development that JLL track is 21% lower over the past year and a massive 46% below its late-2016 peak.

“The bottom line is the amount of apartments being built will continue to fall for some time yet and will fall below the level of underlying demand from population growth. This will allow the market to catch up and fully absorb recent strong construction levels," said Mr Warner.

"However, ultimately I think it will mean not enough new rental stock coming into the market over the next few years and we’ll see vacancy return to tight levels and quite strong rental growth start to emerge in 18 months to two years’ time.

“This won’t be good news for lower-income renters, while it is likely to further extend the time to accumulate a deposit for younger aspiring buyers. Nevertheless, a silver lining is that a surge in rents might prove to be a strong catalyst for our political leaders to get behind build to rent residential more unequivocally and reduce some of the taxation and regulatory hurdles currently inhibiting its emergence,” he said.

The number of apartments under construction in Inner Sydney fell 17% to 10,230 in 2Q19 and is 40% lower than a year ago. The number being marketed has fallen 57% over the past year and the total supply pipeline tracked at all stages of construction is just under half its peak level in late 2017.

Source: JLL Research

Further, supply under construction in inner Melbourne fell 3% in the quarter to 17,960 apartments, down 9% over the year. Against the trend of the past year when a number of projects have stopped marketing and flipped to alternative uses, the number of apartments marketed in Inner Melbourne rose slightly in 2Q19 to 8,180.

“Like Sydney, confidence appears to have returned to the Melbourne housing market in recent months and prices appear to be stabilising,” said Mr Warner.

Source: JLL Research

Yet, just 4,350 apartments were under construction in inner Brisbane at the end of 2Q19, which compares to a peak of just under 16,000 in 2016. The number of apartments being marketed rose slightly to aroundv1,180, but this is still 68% lower over the past year and 85% lower than its 2016 peak level.

“Like Brisbane, Perth appeared to be stabilising in 2018 but slipped backwards in the cycle slightly over the first half of 2019, with price declines accelerating once again as credit conditions and negative sentiment nationally impacted the market,” said Mr Warner. “However, WA’s economy is inching its way toward recovery and population outflows have been stemmed."

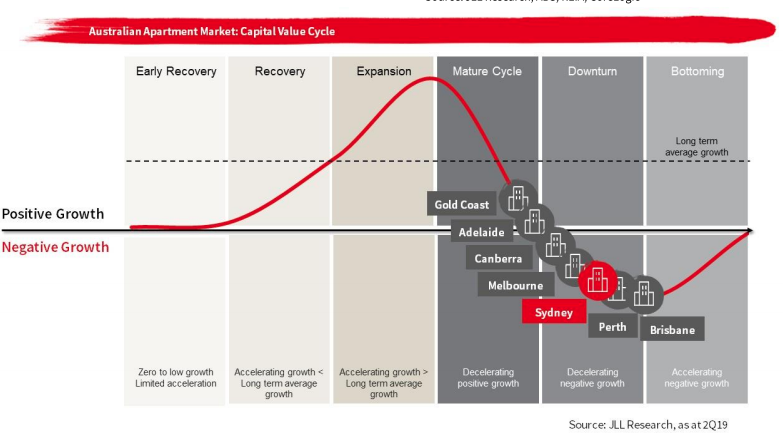

Mr Warner also said that neither Adelaide nor Canberra have historically had significant apartment markets, but apartment living has started to take off in both markets over recent years.

"Supply levels remain elevated in both markets, which will put some moderate pressure on pricing ahead, but solid economic prospects and improved market sentiment after the interest rate cuts and easing of credit constraints is likely to mean a shallow downturn for Adelaide and Canberra," he said.

Click here for more analysis from JLL Research.

Similar to this:

Low maintenance and safety the focus for Australian apartment owners, survey says

Apartment disasters driving buyers to detached housing, says Thrive Homes

Lower investor demand reflected in shrinking apartment pipeline - JLL

Contact Details: