Building activity hits new low, says report

Contact

Jul 29, 2019

Building activity hits new low, says report

The combination of tougher lending practices and falling property prices has been a big hit to new property demand, according to BIS Oxford Economics.

-

BIS Oxford EconomicsBIS Oxford Economics Managing Director Robert Mellor.

BIS Oxford EconomicsBIS Oxford Economics Managing Director Robert Mellor.

New building commencements are expected to hit a low in the 2019/20 year, before recovering strongly by 2020/21, according to BIS Oxford Economics.

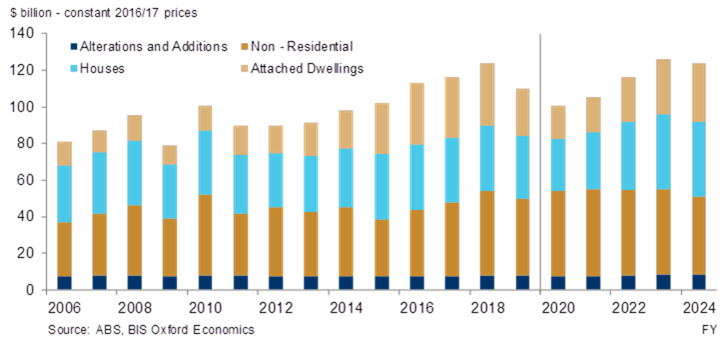

The real value of national building commencements contracted an estimated 12 per cent in 2018/19 to $109.8 billion (in constant 2016/17 prices), from the record peak reached the year prior, according to the company’s Building in Australia 2019-2034 report.

“FY2019/20 should represent the trough for total building, with a strong rebound anticipated from 2020/21 onwards as interest rate cuts, easing mortgage serviceability tests and first home buyer stimulus help facilitate a broad recovery,” said Robert Mellor, Managing Director, BIS Oxford Economics. “Total building activity is anticipated to climb near its previous peak over the coming five years."

At a glance:

- New building commencements are expected to hit a low in the 2019/20 year, before recovering strongly by 2020/21, according to BIS Oxford Economics.

- Victoria (-23 per cent) saw the largest decline following a record peak the year prior, as the correction underway in New South Wales picked up the pace, falling 14 per cent.

- “From somewhat of a balanced position, Australia’s dwelling stock deficiency will grow once again as rising undersupplies in Victoria, Queensland and Tasmania develop by 2020/21,” said Mr Mellor. “We anticipate this pressure to facilitate growth in house prices and rents, helping create a renewed upswing in residential building starts through the early to mid-2020s.”

But the downturn has further to run with an additional eight per cent decline forecast for 2019/20, with the fall in residential building outweighing the growth expected in the non-residential sector.

The report also highlighted that the combination of tougher lending practices and falling property prices has been a big hit to new property demand. The premium that is paid for new property makes it especially sensitive to negative price growth.

Value of total building commencements. Source: BIS Oxford Economics

“Strong population growth, a rising national dwelling stock deficiency and housing stimulus are set to provide considerable support to the residential building and renovation sectors, while the non-residential building is projected to remain elevated at a high base over the medium term,” said Mr Mellor.

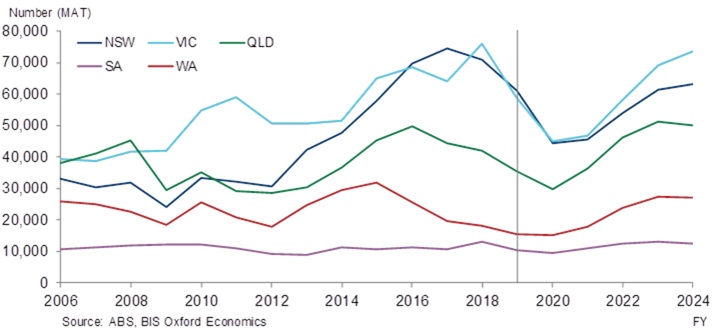

A residential downturn is well underway, with the number of total dwelling commencements contracting in 2018/19 by an estimated 16 per cent to 191,800. Attached dwellings are estimated to have declined 24 per cent, while houses declined a more modest nine per cent.

However, not all states and territories were in the red, with Tasmania (+17 per cent) and the ACT (+22 per cent) offsetting some of the falls elsewhere in total dwelling commencements.

Victoria (-23 per cent) saw the largest decline following a record peak the year prior, as the correction underway in New South Wales picked up the pace, falling 14 per cent.

Total dwelling commencements by state. Source: BIS Oxford Economics

The national rate of property turnover has dropped back over the past two years, in line with falling house prices. Tighter lending conditions triggered by the Banking Royal Commission battered buyer confidence and restricted access to finance.

Land sale volumes in most key greenfield markets have fallen back sharply over the first half of 2019 and off-the-plan apartment sales have also been running at a very low level. This has baked in the current downturn, given the lag time to construction.

It is not until mid-2020 that a suite of stimulus measures are expected to positively flow through to new dwelling construction by facilitating credit availability, reducing barriers to entry and boosting confidence.

This environment will help propel the next upswing. These measures include lower housing interest rates with a further rate cut expected in December quarter 2019, the removal of the seven per cent mortgage serviceability floor by Australian Prudential Regulation Authority (APRA), and the Federal Government’s First Home Buyer Deposit Scheme.

Related reading: Brisbane expected to record biggest rise in house prices, says report

Despite the severity of the downturn (33 per cent decline from peak to trough), national residential commencements will trough at 152,900 dwellings – a historically elevated level. This trough is well above the average of prior cycles back to the 1970s.

“From somewhat of a balanced position, Australia’s dwelling stock deficiency will grow once again as rising undersupplies in Victoria, Queensland and Tasmania develop by 2020/21,” said Mellor. “We anticipate this pressure to facilitate growth in house prices and rents, helping create a renewed upswing in residential building starts through the early to mid-2020s.”

Over the four years to 2023/24, given this pressure in the market, dwelling commencements are forecast to rise a cumulative 55 per cent to a peak of 236,650 in 2023/24. This new record level is projected to be the peak of the cycle.

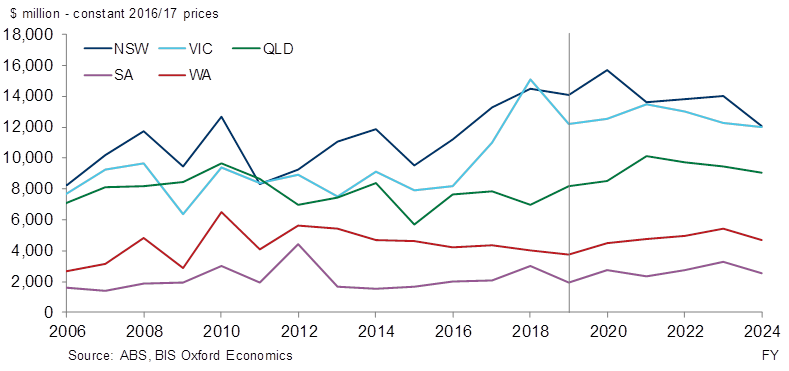

New South Wales and Queensland will lift to record levels in non-residential building over the next two years. Continued tightness in the Sydney office market should enable this sector to continue running at a high level, while a significant pipeline of major projects across defence, health and hospitality will support the Sunshine State.

Total non-residential building commencements by state. Source: BIS Oxford Economics

“Combined with strong population growth, tightness in some asset classes and most importantly a strong project pipeline, the non-residential outlook remains favourable,” said Mr Mellor.

It is anticipated that non-residential building activity will remain near this high base until 2022/23. Relatively stable economic conditions continued solid population growth and a series of large-scale transport infrastructure projects across the nation will help fuel investment.

Defence projects such as the Australia-Singapore Military Training Initiative and a string of major hospital developments – including the $1 billion New Footscray Hospital – look set to provide considerable support.

“Halfway through the residential downturn, our sights are now set on the recovery. The next pick up in new dwelling construction is expected to coincide with a continued buoyant level of non-residential investment and a turn in mining investment,” said Mr Mellor.

“Queensland and Western Australia are well-positioned to lead the next residential upturn, ahead of New South Wales and Victoria.”

First home buyers and upgraders will initiate the recovery in residential commencements. As pressure on the dwelling stock increases, rental vacancy rates will tighten, and rental growth should accelerate. Once gross yields for residential property appear more favourable, investor demand is expected to start firing for both new and existing dwellings, but this is unlikely to occur until the second half of 2021.

However, if investors do not return to the market as expected, the momentum needed to sustain the recovery will be lacking.

“We could experience a deeper downturn before then, and delayed recovery if fundamental drivers of residential activity were to ease more than expected,” said Mr Mellor.

“A crisis of confidence surrounding build quality in the apartment market has the potential to weigh further on apartment construction over the short term, adding downside risk to the outlook.”

Click here for more analysis from BIS Oxford Economics.

Similar to this:

Housing downturn 'should not be overstated', says CBRE economist

Is construction sector really facing "biggest fall since GFC"?

Contact Details: